Sports as an Asset Class: The Hidden Outperformer in the Private Markets

Why investors are starting to take sports seriously, and what the data shows about its risk, return, and future upside

Summary

Sports franchises have compounded at 13.1% annually for over 60 years, outpacing equities with lower volatility and near-zero correlation

Beyond franchises, growth is accelerating across youth leagues, women’s sports, streaming, and fan engagement infrastructure

As global demand, monetization tools, and governance evolve, sports are transitioning from a niche passion play to a core private market allocation

Once reserved for an exclusive club of billionaires and celebrities, sports have evolved into a legitimate, high-performing asset class, now attracting even the most traditional institutional investors. As barriers to investment have loosened, the market has begun to recognize how sports deliver superior long-term returns, stable cash flows, and low correlation to broader market cycles. As its exceptional track record has expanded institutional interest, franchises and the broader sports ecosystem now compete directly with private equity, real estate, and other alternatives for space in long-term portfolios.

While non-financial factors like fandom and prestige may add emotional appeal, what’s primarily driving the increased capital allocation is the numbers. According to the Ross-Arctos Sports Franchise Index, North American franchises have compounded at 13.1% annually since 1961, outperforming public equities by 2.6% per year with lower volatility and near-zero correlation to macro cycles. As sports secures its place as one of the top-performing private asset classes, it’s worth exploring this category’s investment properties, return dynamics, and where the next wave of value may come from.

Measuring the Market: What RASFI Tells Us

The RASFI index, developed by the University of Michigan’s Ross School of Business in partnership with Arctos Partners, offers the clearest quantitative outlook on long-term franchise value growth. Based on over 445 franchise transactions dating back to 1923 across the NFL, NBA, MLB, and NHL, RASFI uses actual deal comps and revenue multiples to provide transparent and real-time pricing data, which is especially valuable in a markedly opaque private market.

As shown in the chart below, sports franchises have outperformed every major asset class over the past 60+ years. While billionaires purchasing stakes in their favorite teams would be content knowing their investment outpaces inflation, sports franchises’ consistent outperformance over equities by around 2.6% annually is what has drawn serious attention from institutional investors and non-sports allocators.

Although high returns are appealing, outperformance alone does not make an asset class compelling, as institutions must also heavily consider volatility and downside protection. However, looking at sports’ risk-adjusted return makes the asset class even more impressive. In the risk/return chart below, RASFI stands apart by delivering higher returns than venture capital, private credit, and even the traditional 60/40 portfolio, all while maintaining lower volatility. The combination of first-rate returns and minimal risk is rare and increasingly attractive in a market environment where capital efficiency and downside resilience are preeminent.

This risk protection shows up clearly in real-time data. In its most recent Q4 2024 report, RASFI rose 2.9% for the quarter and 17.3% for the year, handily beating out private equity (7.3%) and private credit (8.2%), though trailing US equities, which posted a rare 25% rally. Over time, the RASFI has demonstrated significantly smaller drawdowns than public markets, with far fewer periods of steep decline. This resilience makes the asset class especially valuable for portfolios prioritizing capital preservation without sacrificing upside.

Why Sports Franchises Compound Like Few Other Assets

There are three primary forces that drive long-term franchise value: media rights renewal shocks, wealth accretion across the economy, and the continued rise of the experience economy.

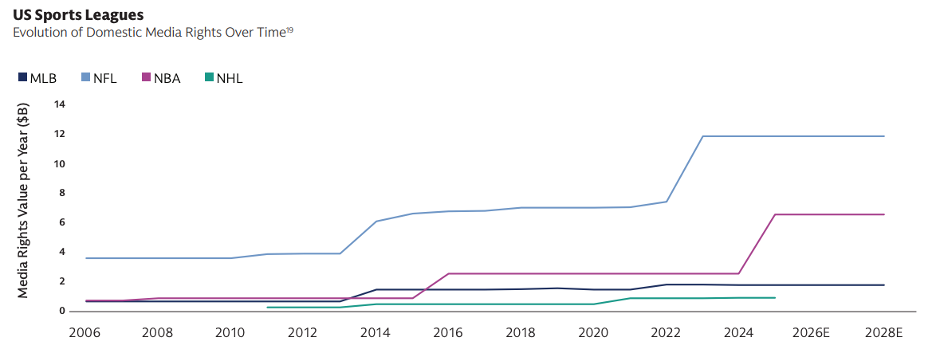

When leagues lock in new national broadcast or streaming deals, the entire valuation base resets. In 2023, the NFL signed an 11-year, $110 billion rights agreement with CBS, NBC, Fox, ESPN, and Amazon. That deal now funnels over $400 million annually to each team, making media rights responsible for more than 60% of total league revenue. These infrequent but powerful shocks create structural tailwinds that lift all boats, especially in US leagues, where revenue is distributed equally across franchises. As shown in the chart below, the NFL and NBA have seen substantial rights value increases following their most recent renewals, continuing a long-term upward trend.

On the other hand, European leagues have struggled to sustain growth. France’s Ligue 1, for instance, suffered valuation setbacks after a failed media rights deal with Mediapro. This divergence has widened the valuation gap between U.S. and European franchise values and forced European teams to explore alternative monetization paths, such as direct-to-consumer platforms and personalized fan engagement. Research shows engaged fans spend up to six times more than casual fans, making first-party data and digital infrastructure increasingly critical. In North America, the combination of long-duration media deals, stable governance, and equitable revenue distribution has created a steady floor for franchise valuations. While media rights remain a dominant driver, investors should be mindful of potential saturation. If domestic rights values experience a plateau like the stagnation seen in parts of Europe, franchises and the broader ecosystem will need to innovate around owned IP, streaming control, and diversified fan monetization.

The second major driver is wealth accretion. As global wealth expands, so does the demand for rare and culturally significant assets. With a fixed number of teams, structural demand from buyers, and strong recurring revenues, sports franchises increasingly resemble long-duration, yield-generating real assets. The recent minority sales of the Eagles, Bills, and Dolphins at multibillion-dollar valuations reflect this dynamic. Although some believe these rising valuations are irrational, the asset class’s historical non-correlation, inflation resilience, and income durability continue to justify long-term capital allocation.

Lastly, sports are thriving within the broader experience economy. In a world where consumer attention is fragmented and digital platforms increasingly dominate, live sports remain one of the few remaining forms of real-time, communal engagement. Leagues own the content, control distribution, and monetize across a wide spectrum from premium advertising to digital channels. Franchises have evolved into vertically integrated media businesses with assets spanning branded IP, streaming rights, ticketing platforms, ecommerce operations, and fan data infrastructure. A single team can command 80,000 fans in a stadium and tens of millions more on screens, offering advertisers and investors a rare combination of cultural relevance, live engagement, and monetization at scale.

Resilience Without Correlation: A Unique Risk-Return Profile

As mentioned earlier, sports franchises possess an uncorrelated risk profile, one of the key reasons investors are increasingly allocating capital to the asset class. On the surface, franchise economics may seem vulnerable to investors given their reliance on consumer spending. However, that concern fades when considering the remarkable stickiness of fan behavior, especially during broader economic downturns.

For example, despite the COVID-19 pandemic eliminating live attendance in 2020, the NFL still generated over $12 billion in revenue, driven largely by media rights and fan engagement. Just one year later, revenue jumped to a record $17.2 billion and has continued to surge. Contrarily, U.S. airlines took several years to recover and have only since surpassed 2019 revenue once, as shown in the chart below. This contrast underscores how sports revenues, anchored by media contracts, are structurally more resilient than even essential, consumption-driven industries like air travel.

Unlike most discretionary categories, sports consumption is driven more by identity and habit rather than by affordability. People cut back on vacations or dining during a recession, but far fewer are willing to miss their team’s playoff run.

Beyond consumer resilience, sports franchises exhibit consistently low correlation with public equities at around 0.25 to 0.30 over long periods. Other private assets like PE and VC experience sharp valuation resets when public multiples fall, but sports valuations are less reactive due to infrequent transactions and the durability of media-driven cash flows.

Moreover, sports do not follow the same boom-bust cycles that characterize other alternative asset classes like early-stage tech and real estate. Instead, they benefit from macro wealth creation and market optimism while largely avoiding the downside of economic corrections. In other words, sports possess the risk of a bond with equity-like returns, making the asset class a unicorn in the private markets landscape.

A Global, Underpriced, and Expanding Market

Globally, the sports asset class is expanding rapidly and becoming increasingly accessible to all types of investors. While long-term growth is widely expected due to rising global engagement and monetization tailwinds, the real opportunity lies in underpriced and emerging segments across geographies, genders, and business models.

According to Elixirr, the global sports ecosystem reached $463 billion in 2024, with projections nearing $863 billion by 2033. While North American leagues have seen stable revenue growth, the Indian Premier League stands out as a case study in exponential return potential. Team valuations in the IPL have surged from $67 million in 2009 to over $1 billion today, proving that early bets on smaller leagues can produce outsized returns as scale, sponsorship, and media partnerships evolve.

Women’s sports represent another frontier with explosive upside. The 2024 NCAA women’s basketball championship drew 24 million viewers, surpassing the NBA Finals and World Series. Capital is flooding into the space, and valuation gaps between men’s and women’s leagues are closing fast. Youth sports are also drawing increased interest, as firms like TCG have launched Unrivaled Sports, a platform partnering with AAU to consolidate and scale youth basketball properties, aiming to monetize participation, events, and media.

Across the Atlantic, European soccer presents a unique arbitrage opportunity. Clubs in leagues like the Premier League and La Liga have 20 times the social media reach of U.S. teams, yet trade at lower valuations due to relegation risk, governance challenges, and financial instability. As Crystal Palace chairman Steve Parish put it, relegation remains "the biggest financial jeopardy in world football.” However, governance is improving as cost controls tighten and new capital continues to flow into the system. For investors who can navigate the risks, meaningful upside exists to capitalize on potential undervaluations.

Finally, PE firms are increasingly targeting the infrastructure around sports, not just the teams themselves. Growth areas include media platforms, streaming technology, fan engagement software, and sports betting operators, all of which can scale faster and require less capital than owning franchises. RedBird Capital has taken a platform approach, pairing team investments with distribution and monetization layers to build vertically integrated portfolios with asymmetric upside.

The Bottom Line: A Distinct Asset Class Built for the Future

Over the past decade, the case for sports as an asset class has become clear. Long-term return data from RASFI confirms that sports franchises offer best-in-class compounding with lower volatility and downside protection. Institutional capital is now fully onboard, and as league regulations evolve, these investors are increasingly shaping the rules of participation.

As global sports consumption accelerates, and media rights and digital monetization strategies unlock new revenue streams, the value creation potential continues expanding. From legacy franchises to youth leagues, and from streaming platforms to fan data infrastructure, the ecosystem is growing in both scale and investability.

For allocators seeking stable and long-duration assets that perform across cycles, and for entrepreneurs building new tools to understand them, sports are no longer a niche. Over the next decade, I believe sports will become an established alternative private investment, with the smartest investors continuing to lean into one of the most compelling anomalies in private markets.